Call Us -

1800 608 088

Navigating the complexities of Division 7A can be challenging. If you fail to comply with Section 109D you can be hit with severe penalties, including the reclassification of loans as dividends which leads to unintended tax consequences. Our Division 7A Compliant Loan Agreement is meticulously crafted to help your company, its directors, and shareholders meet their obligations and avoid these pitfalls.

Division 7A is a set of rules designed to prevent private companies from making tax-free distributions to shareholders (or their associates) in the form of loans, payments, or debt forgiveness. If these distributions do not meet specific criteria, they may be treated as unfranked dividends, resulting in additional tax liabilities for the recipients.

Section 109N: Specific Criteria for Loans Under Division 7A

Section 109N outlines the specific conditions that must be met for a loan from a private company to a shareholder (or their associate) to avoid being classified as a dividend under Division 7A. Essentially, Section 109N sets the “safe harbor” rules for loans to ensure they are not treated as dividends.

Key Provisions of Section 109N:

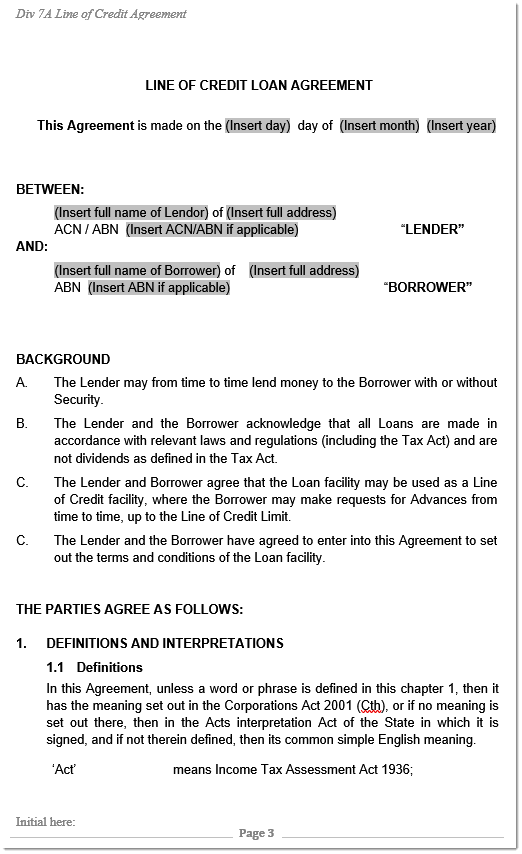

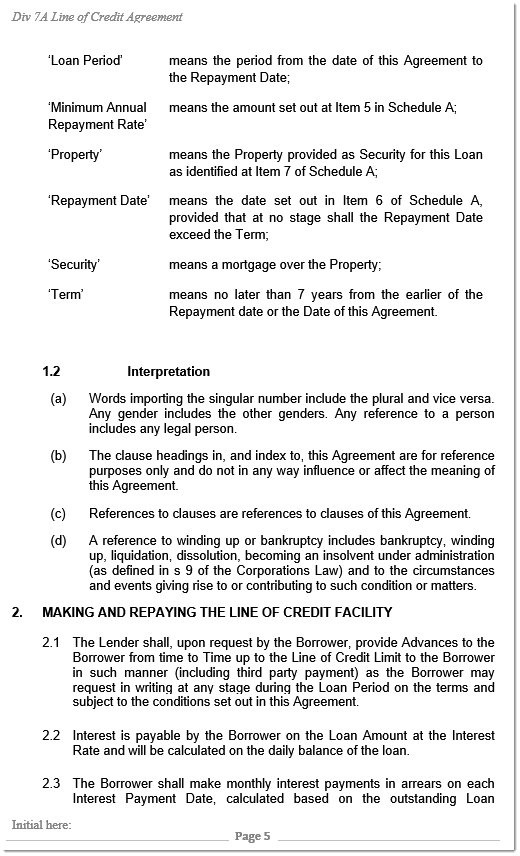

Written Agreement:

The loan must be documented in a written agreement before the lodgement day for the company’s tax return in the year the loan is made.

Benchmark Interest Rate:

The interest rate on the loan must be equal to or greater than the “benchmark interest rate” for that year, as determined by the Reserve Bank of Australia. This ensures the loan is not effectively a gift or disguised distribution of profits.

Maximum Loan Term:

The loan term must not exceed:

When Might You Use This Agreement?

Tax-Efficient Lending for Private Companies

This document will allow you to structure your loan correctly to avoid div7a penalties. It has been professionally drafted by Australian lawyers to meet the requirements of the Income Tax Assessment Act 1936 including those listed above, ensuring your loan won’t be treated as a dividend which could lead to higher tax liabilities.

Flexible Line of Credit with Clear Terms

Directors or shareholders can establish a Line of Credit facility with this agreement, accessing funds as needed, up to a pre-determined limit. You can draw, repay, and re-borrow within the specified term, ensuring you comply with the strict requirements of Division 7A while enjoying the financial flexibility this arrangement provides.

Secure Your Loan with Real Property

If you choose to secure the loan with real property, you can extend the loan term up to 25 years, provided that the property’s market value exceeds 110% of the loan amount and the security is registered. This allows you to leverage your assets effectively while ensuring the loan remains compliant with Division 7A.

Refinancing Options

Our agreement also provides for refinancing existing loans while maintaining compliance with Division 7A. If you’re looking to refinance an existing loan, our agreement ensures that the maximum term is adjusted appropriately, allowing for a seamless transition while avoiding potential tax pitfalls.

Our Division 7A Line of Credit Agreement complies with the ATO’s requirements and allows you to document your loan correctly.

Our template saves you re-inventing the wheel and gives you a cost effective way to meet your obligations.

Buy Div 7a Line of Credit Agreement - Instant DownloadIt is available for immediate download as Microsoft Word document which makes it easy to edit. In addition it can be used as often as you need.

There are other types of Division 7a Loan Agreements which operate like a standard loan where you pay money back rather than having a revolving line of credit. Here is a breakdown of the different loan templates so you can decide which one you need. Or so our article Division 7a Loan Agreements Tax Facts

| Type of Agreement | Loan Term | Secured/Unsecured | Use Case | Flexibility |

|---|---|---|---|---|

| Secured Division 7A Loan | Up to 25 years (secured by real estate) | Secured | Long-term lending needs with collateral | Fixed loan amount, no redraws |

| Unsecured Division 7A Loan | Up to 7 years | Unsecured | Shorter-term loans, no collateral required | Fixed loan amount, no redraws |

| Line of Credit (LoC) | Up to 25 years (secured), 7 years (unsecured) | Secured or Unsecured | Flexible access to funds; ongoing borrowing | Draw, repay, and redraw up to the credit limit |

Our Agreements are drafted to comply with Australian Law

The agreements are professionally drafted by Australian Law Experts

No Need to Wait. Download the Agreements Instantly

Plain English - No Legalese. Your Agreement is easy to use, edit and understand